Why Flagler’s Home Prices Were Slow To Recover And Why That’s About To Change

New home construction has not been enough to absorb Flagler’s growing population, but unoccupied distressed homes covered the construction deficit. Now that secondary source is quickly disappearing.

PALM COAST, FL – June 2, 2016 – I was quoted in a June 2011 article <story> in the Washington Post saying, “Flagler County is the poster child for what went right and what wrong in the economy.” Flagler was the housing bubble on steroids. For two years running, Flagler County and Palm Coast respectively were the fastest growing county and city in the U.S.

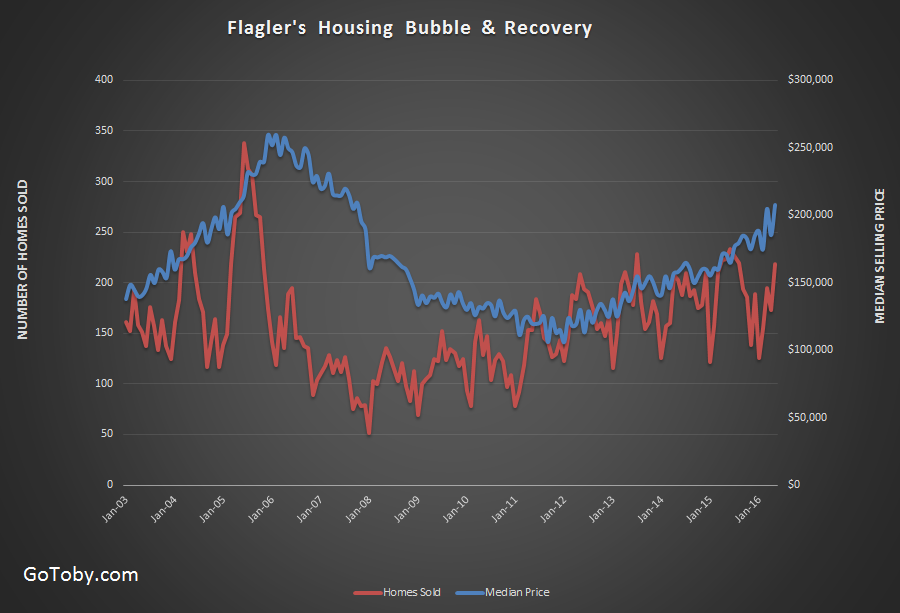

Flagler’s housing bubble led the rest of the nation with prices rising sooner, rising higher (in percentage terms), peaking sooner, falling more precipitously, and bottoming at a lower level. The median selling price for a single-family home fell more than 60%.

But Flagler’s housing market did not lead the nation’s recovery. Recovery has been slow. Home sales began to rise again in 2008, but prices continued a downward slide until 2012 before turning upward again. While other regions have rebounded to pre-recession highs, Flagler County median home prices remain roughly 20% below the 2005 peak of $259,950.

The Housing Bubble and Recovery in Flagler County

Flagler’s housing bubble was driven primarily by investors and speculators, not by an underlying demand for housing. The investors/speculators did not plan to occupy the home. They simply planned to turn around and sell the property at a profit to the next person in line. When the bubble burst, Flagler was terribly overbuilt. Spec homes dotted the landscape. This bloated inventory of unoccupied homes and condos became the source for the short sales and foreclosures of the next several years. From 2009 through 2011, distressed home sales accounted for more than 50% of all home sales in the county.

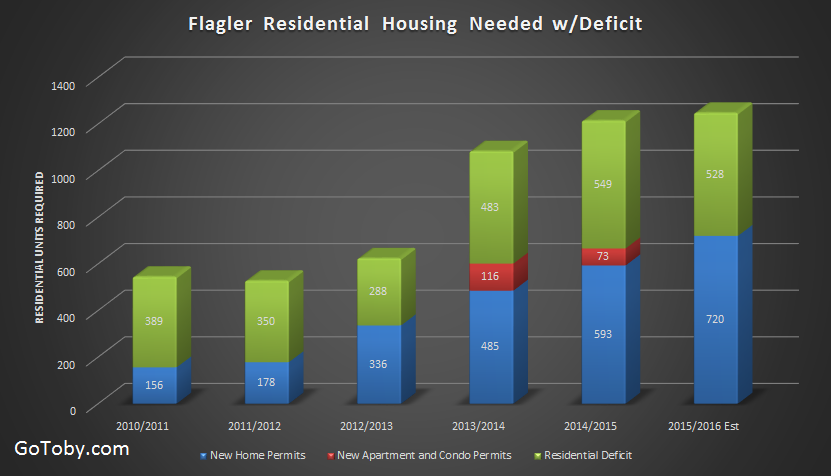

Flagler’s population has continued to grow, expanding by 10% between 2010 and July 2015. And the population growth rate is accelerating. A recently released U.S. Census Bureau report estimates the county added 2,831 new residents between July 2014 and July 2015, a 2.76% gain. That was enough to place Flagler 64th on a national list of fastest growing counties with populations over 100,000.

When planning for growth, the Flagler County School District estimates 2.33 residents per household. (The national average is 2.54, but Flagler has more retirees, thus fewer children). Therefore, adding 2,831 new residents creates a need for an estimated 1,215 new residential units (condominiums, homes, apartments). Yet, new home construction has not kept up the pace. Only 545 residential building permits were issued during 2014 and 583 in 2015. Building permits are on track to total more than 600 and perhaps even 700 units in 2016, but Flagler will have created a need for another 1,248 residential units with the July 2015 to July 2016 estimated population gain (based on the same 2.76% rate as July 2014 to July 2015.)

The Drop in Distressed Home Sales Drives UP the Housing Deficit

.png)

Two questions come to mind:

- Where are all these new arrivals living, since not enough new homes have been built?

- Assuming continued growth, where will future arrivals settle?

Move Out – Move In

When one family moves out and another moves in, there is no increase in population, therefore no additional residential units are required. New additions to the population have to find an unoccupied home; and at a rate of one home for each 2.33 net additional residents. The inventory of unoccupied homes consists of new construction, foreclosures and vacant short sale units. The following graph illustrates a new construction deficit over the most recent six years. Data for the year ending July 2016 is estimated.

Now Home Construction Is Increasing, But So Too Is Flagler's Population

The deficit shown in the chart did not translate into rapid price increases because there was a continuing supply of unoccupied distressed properties to take up the slack. Home sales were brisk, but median prices in the Flagler market rose more gradually than in many other regions.

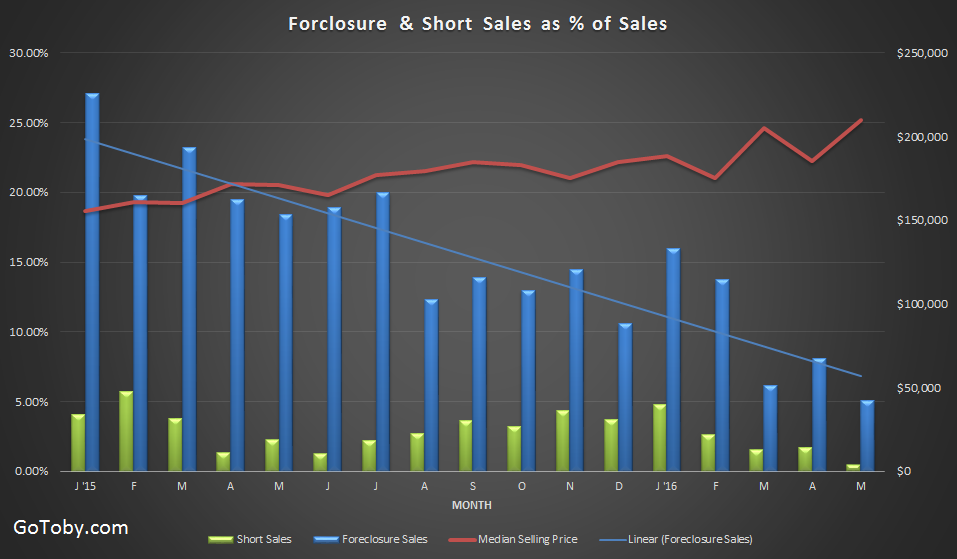

Short sales have been in decline for many months, becoming an irrelevant sector several months ago, but Florida’s judicial foreclosure system continued to feed additional properties into the unoccupied foreclosure inventory; until recently. The graph shows the dramatic change in product mix since January 2015, when distressed sales accounted for 31.2% of all home sales.

Foreclosure Sales No Longer Cover The New Home Construction Deficit

The well is nearly dry. There will be an insignificant level of distressed inventory going forward, leaving new construction as the only option for Flagler’s growing population. If new construction can keep up the pace, price increases will be more moderate. To the extent that an inventory deficit remains, the excess of population-driven demand over supply will accelerate price increases.

Local builders complain about the shortage of skilled and unskilled construction workers, even at the current rate of construction. There is no short-term fix to the labor problem. Labor shortages will continue to exacerbate the construction deficit in the near future, accelerating the pace of rising prices. As home prices rise, so too will rentals.

The dramatic drop in distressed home sales and the concomitant increase in traditional sales is sustainable. In May, distressed sales accounted for only 5.5% of all home sales and only 4.0% of total sales value. But what about the pipeline. 769 single-family Flagler County homes are currently listed for sale through Flagler MLS. Only six are short sales and ten are foreclosures, totaling only 2% of total listings.

There has been some concern that home sales have dropped off somewhat from one year ago. The concern is not surprising. We have gotten used to monthly year-over-year gains in home sales, but in five of the past seven months, home sales have dropped year over year.

Through May, total home sales in 2016 are off 7.0% (66 homes) from the same period one year ago. But distressed sales during the same periods dropped from 227 to 95 (58.1%). Disregarding distressed sales, traditional sales have increased over the first five months of 2016 by 9.3%. The dollar value of traditional sales increased a very healthy 15.7% over the same period.

Someone here is on Top of things!!!

Just a quick note to say that I read many of your articles and enjoy them being that they are so informative. I am glad to see someone here is on top of things and has statical knowledge of what is going on here in Palm Coast. Most people that live here want to know what is going on in their neighborhood and have no where to look. You have just filled that void. Thank you very much and please keep these articles coming.

Sincerely,

Edwin Aviles

Palm Coast’s unsustainable housing bubble of it’s

I’m happy you acknowledged why Palm Coast was growing so disproportionately to the demand by any influx of families.

I totally agree and suggest that the newspaper headlines of that time should have more accurately read ‘Palm Coast, The Fastest Growing Community Of EMPTY HOMES in America.’

Sadly what your piece did not acknowledge was the part played by Realtors, Builders and Real-Eastate Lawyers whom were all in a position to know the facts that this was an out of control speculation driven boom that grossly exceeding the true growth rate.

Without any doubt, if investors were informed the truth that 70-90% of all new construction at that time was SPECULATOR AND INVESTOR OWNED………. AND SITTING VACANT many would have figured it for themselves and withdrawn.

The reality is that the causes & blame for Palm Coast’s devastating “Housing Bubble Crash” and legacy of that crash can be spread much further than pointing solely towards “investors and speculators”.

Reply to Brian

Your implication that the Realtor and builder community should have informed buyers about the reality of the market is built upon a false premise; that they, themselves knew about the dangers in advance. In fact, the roles of foreclosures, bankruptcies and even divorces and suicides brought about by the housing collapse is strewn with names of Realtors, builders and developers alike. Further, it’s unrealistic to expect those in the industry to have forecast a housing recession unheard of in its suddenness, its depth and its duration.

There is plenty of blame to go around. Just look at all the people involved in each transaction; the buyer, the buyer’s agent and broker, the seller, the seller’s agent and broker, the appraiser, the title company, the inspector, the builder, the developer, the loan originator, the lender, the Wall Street banker, the hedge funds, the pseudo government guarantors and the federal government itself.

Blaming the industry for causing real estate speculation is like saying that casinos cause gambling when, in fact, casinos are built because gamblers already exist.