Real Estate Stats Losing Credibility

There are too many outside influences affecting real estate sales. Monthly numbers have less and less to do with underlying market conditions.

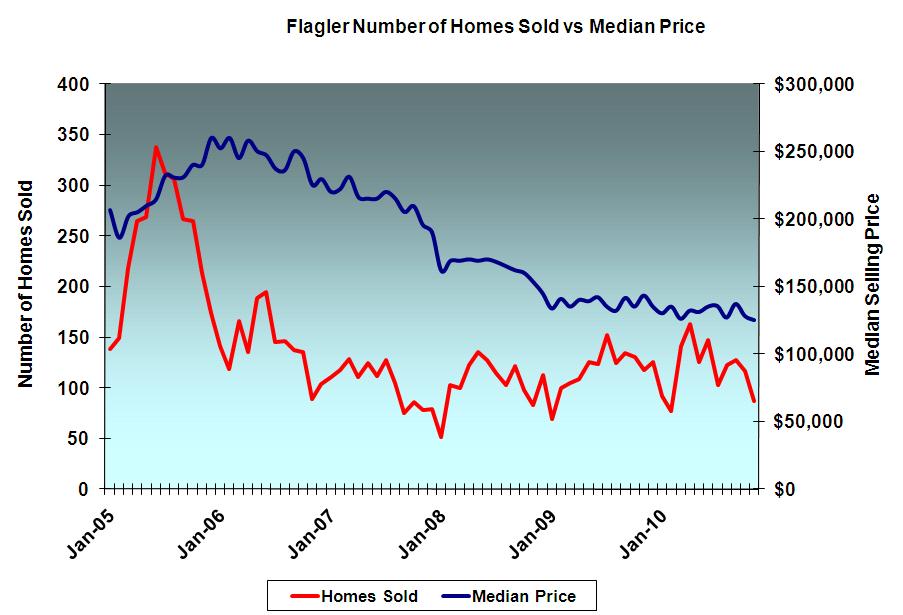

Palm Coast, FL – December 6, 2010 – I’ve always watched numbers (and graphs and charts) for early indications of market changes and to determine trends, but too many outside influences are messing with the data these days. The simple Supply vs. Demand analysis doesn’t work as well anymore. When prices went down, it was because of either reduced demand or increased supply. When more buyers wanted new homes, more building permits were issued. Lower mortgage interest rates still means lower monthly payments and more affordable homes. Increased affordability resulted in more home purchases, more new home construction, and increased refinancing. But not today. The housing and financial markets are being tugged and pulled by so many new factors; traditional analysis has become increasingly speculative.

In Flagler County, 117 single-family home sales were reported closed through MLS during October compared to 127 in September and 130 in October 2009. Only 87 homes have been reported sold in November (the numbers are still trickling in) compared to 118 in November 2009.

The first-time homebuyer tax credit was on the table during this period last year. This year it’s not. So this year’s drop over October and November ’09 is not meaningful, especially since October sales averaged only 106 homes in the three years from 2006 to 2008. November sales averaged only 83 homes per month during the same three years. Normal seasonality accounts for the September to October drop. The fourth quarter plus January are traditionally slow months for real estate closings. October sales have fallen slightly short of September sales in four of the last five years. November sales were less than October in every one of the five years.

Tracking foreclosure filings and foreclosure sales is likewise problematic. The sheer volume of foreclosures exposed the lending industry’s utter failure to cope. Lenders got caught illegally creating documents out of thin air. There are so many foreclosures being cancelled and refilled that the Clerk of Courts cannot keep up. Deed and foreclosure filings are running more than two weeks behind. It has been over a month since a schedule of foreclosure sales has been posted on the Clerk’s website.

Reacting to some of the loose appraisal standards that helped fuel the housing boom, the government overreacted. New appraisal guidelines often result in out-of-town appraisers, unfamiliar with the local housing market, setting local values for prospective lenders. Many think that current appraisals are unfairly affected by the preponderance of REO (lender owned) sales and short sales. Adjustments are supposed to be made, but often are not. Some local builders have told me that they have plenty of interest but that they lost sales because the appraisal did not support new construction costs. The demand is there, but building permits are not.

Finally, mortgage interest rates are at their lowest level in years. A rush to refinance at such historically low rates should be the expected result. Unfortunately, the low rates coincide with the tightest lending standards in recent history. First, it’s hard to refinance when you are underwater. Second, new lending standards rule out so many other applicants.

Outside influences will continue to affect the housing market. As Washington and Wall Street react to each real or perceived threat (economic or political), the housing market will likely be the victim of unintended consequences. Here are just a few possibilities:

The deficit reduction committee’s report suggests doing away with the mortgage interest tax deduction. I don’t think it will happen, but if it did, home ownership will become more costly.The Federal Reserve recently floated a suggestion to change the rescission rights of the 1968 Truth in Lending Act which was originally passed to protect the elderly from predatory lending. Now homeowners are using the rescission clause to fight foreclosures. Apparently this has become too inconvenient for lenders.The missing, lost, or fraudulent document problem has exposed the weakness and inefficiency of our present mortgage servicing and foreclosing processes. The documentation problem is very complex and defies a simple solution. It affects millions of mortgages. It was created by the lending industry, not the borrowers, but it’s the lenders who are receiving the bailout funds.Mortgage servicing companies are being accused of stringing out foreclosures to maximize fees and "default" interest rates.Tax consequences can be a consideration when timing real estate transactions, both residential and commercial. Taxes also affect ownership costs. There are only 26 days left till the expiration of the Bush era tax cuts and nobody can say for sure what will happen. Uncertainty is another thing that affects home buying and real estate investment decisions.Fannie Mae and Freddie Mac are submitting repurchase requests to lenders for mortgages that have defaulted and were not written to fit GSE guidelines. Fitch Ratings estimates banks’ total buyback exposure to all investors may range upward to $180B. They will not acquiesce willingly. Don’t look for a quick solution to the documentation issue. A graduating high-school senior (class of 2011) will have time to pursue pre-law and law degrees plus pass the bar exam in time to catch the tail end of this saga.As the Fed pulls extra liquidity out of the money market, mortgage interest rates will rise. We have probably seen the bottom. Although record low rates did not express themselves in increased home sales, rising rates will likely show their effects by putting a damper on sales and price gains.If it turns out that faulty documentation was the basis for a foreclosure, it will be the title insurance companies who are on the hook. These companies have already started to rattle their sabers at lenders, trying to put off future exposure onto lenders. But the title company vs. lender battle will spill out into the real estate community at large. Traditionally location, location, and location have been the three most important factors of real estate value. That may change to clear title, clear title, and clear title. If so, mortgage-free homes and those with a clear title paperwork trail might sell more easily and demand premium prices.Values in many deed restricted communities, especially condominium communities, are depressed. Excessive unpaid association assessments, vacancies, and foreclosures prompted lenders to refuse purchase mortgage financing within affected communities, limiting the potential buyer pool to those with cash or private financing. The result is even lower values which, in turn, create more foreclosures, etc. This cycle will persist until a healthy buyer market appears. Opportunities abound for the savvy buyer but beware of the risks.

Lenders income is very dependent on interest rates. That’s why they offer lower rates for Adjustable Rate Mortgages. They know they will be protected over the life of the loan from interest rate fluctuations. On the other hand, borrowers’ income is only slightly dependent on interest rates. Borrowers prefer the stability of the fixed monthly payments that come with Fixed Rate Mortgages.

I recently came across an interesting mortgage interest rate twist that helps satisfy both lenders’ and borrowers’ concerns. It accounts for interest rate fluctuations while keeping monthly payments constant. Interest rate fluctuations are addressed by changing the term of the loan, not the monthly payment. As rates rise or fall, the term is adjusted so that the balance of the loan is amortized at the same fixed monthly payment amount. Terms would become shorter when rates fall and longer with rising interest rates. I like it. I hope it becomes a standard offering.

Leave a Reply

Want to join the discussion?Feel free to contribute!