Reading Real Estate Tea Leaves

Predicting the future of the real estate market is not easy.

Palm Coast, FL – October 22, 2010 – In a question and answer session at the annual Charles Schwab Impact conference in Washington on November 6, 2006 Alan Greenspan, former Federal Reserve Chairman said "The economy is obviously going through a significant slowing period, which as best I can tell is more than likely temporary."

While the housing market is not out of the woods yet, the current slump may not worsen, said Greenspan. He also indicated that he expected ARM adjustments to cause some individuals problems, but they were "very unlikely to have a macro-economic effect."

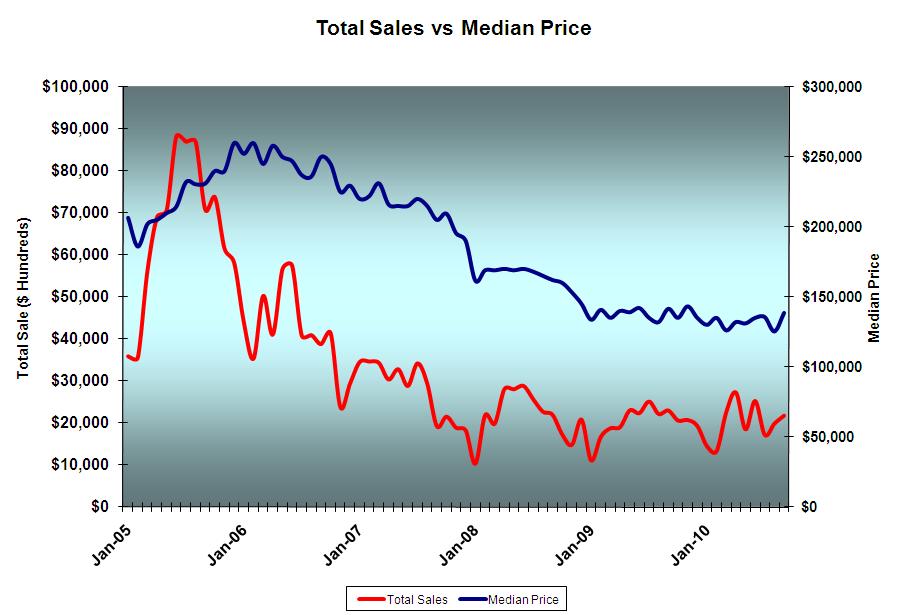

When Greenspan spoke, the median selling price for single-family homes in Flagler County (MLS) was $225,000. Last month, nearly four years later, it was $138,501. That’s a drop of 38.44%. Alan missed the mark.

The median selling price has remained in a fairly narrow range since January 2009. It seemed safe to project a continuation of current conditions until the inventory of distressed properties began to lessen. Then along came the foreclosure documentation crisis. Predicting the future of the real estate market is not easy.

Foreclosure Documentation Crisis

We’ve gotten more efficient at handling distressed property sales. Now the foreclosure documentation mess has thrown a monkey wrench into the works. Some banks have gone so far as to suspended foreclosures. Others will certainly examine documents more carefully, slowing the process. Flagler County Clerk of Courts Gail Wadsworth reports that as many as two thirds of recent foreclosure filings are being withdrawn, probably because the validity of the underlying documents is suspect.For the past two years, distressed property has represented more than half the total number of homes sold locally. Of September’s 119 homes sold, 27 were REO (bank owned) and 41 were short sales. Any actions taken by lenders that will interrupt the distresses sales will reduce supply, altering the market.

Most reactions to the documentation dilemma have focused on foreclosure sales. If the foreclosure is invalidated, title companies may have to pay for the damages. They are becoming leery of their exposure to future challenges.

Most loans made in 2005 and later could be procedurally suspect. Even if a mortgage is older, a subsequent home equity loan or refinancing may be infected with risk. Can the foreclosing lender prove that they own the note and mortgage? If not, they cannot foreclose.

The problem is not limited to foreclosures either. Short sales share the same exposure. In a short sale, the lender agrees to allow a sale price less than the amount owed. They release the lien, allowing the sale to proceed. But if lenders cannot prove they own the note and mortgage, they cannot legitimately release the lien.

Even a standard sale can be problematic. Any sale involving a release of a recently originated mortgage lien can raise red flags for title insurance companies. If they become gun shy, homes with "clear title" will stand out in the market. That means debt free homes or homes with well documented mortgages will be more desirable. If that happens, they will command higher prices.

A Complicated Solution

The documentation problem will take time to fix. Foreclosures are very labor and paperwork intensive. The banks will sort out the problems, but it will take a long time. There’s bound to be extensive lawsuits as well. Watch the Chris Whalen interview on Bloomberg. Chris describes the problems concisely although one problem he identifies – the effect on property tax collections – will likely not affect Florida as much as other states. The Florida system of selling tax certificates (tax liens on delinquent taxes) funnels revenue to taxing authorities quite efficiently.

Recent Palm Coast and Flagler Home Sales

As the graph shows, the local market for single-family homes has remained stable for nearly two years. Prices remain in a narrow band while sales volume shows slow but steady gains.

Foreclosures

Overall, foreclosure filings were decreasing; even before the documentation problems surfaced. Foreclosure of high value properties continues to feed a supply of distressed properties within that sector. Distressed properties bring prices down to a level at which buyers can be found. That trend will continue. There were 56 condominium sales during the third quarter 2009. In the third quarter 2010, the number of units sold climbed to 84 while the median selling price dropped from $313,038 to $202,500. High-end foreclosure filings in September included:

Aliki Gold Coast – one townhome

Bella Harbor – one condo

Canopy Walk – two condos

Cedar Island – one vacant lot

Cinnamon Beach – two vacant lots, one condo

Cypress Hammock – one vacant lot

Hammock Beach – one villa condo, one Beach Club condo

Harbor Side Village – one condo

Marina Cove – one condo

Ocean View Manor – one condo

Palm Coast Plantation – one vacant lot

Sugar Mill Plantation – one home

Tidelands – one vacant lot, four condos

Yacht Harbor Village – two vacant lots

Become a Member of GoToby.com: Receive email notices of news, rumors, newsletters, and articles. [click here] It’s free.

Leave a Reply

Want to join the discussion?Feel free to contribute!