Palm Coast Home Sales Momentum Continues Through July

Three consecutive months of year-over-year sales growth.

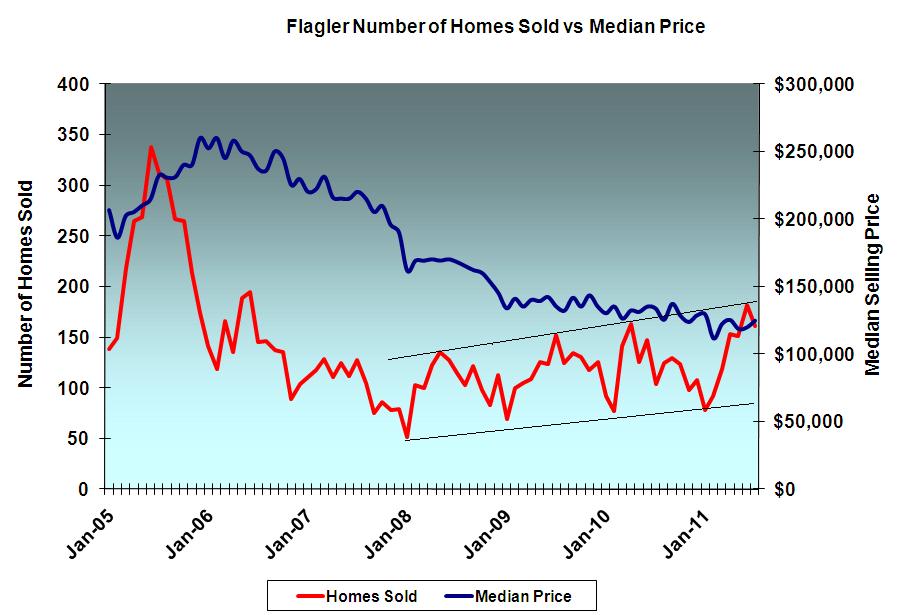

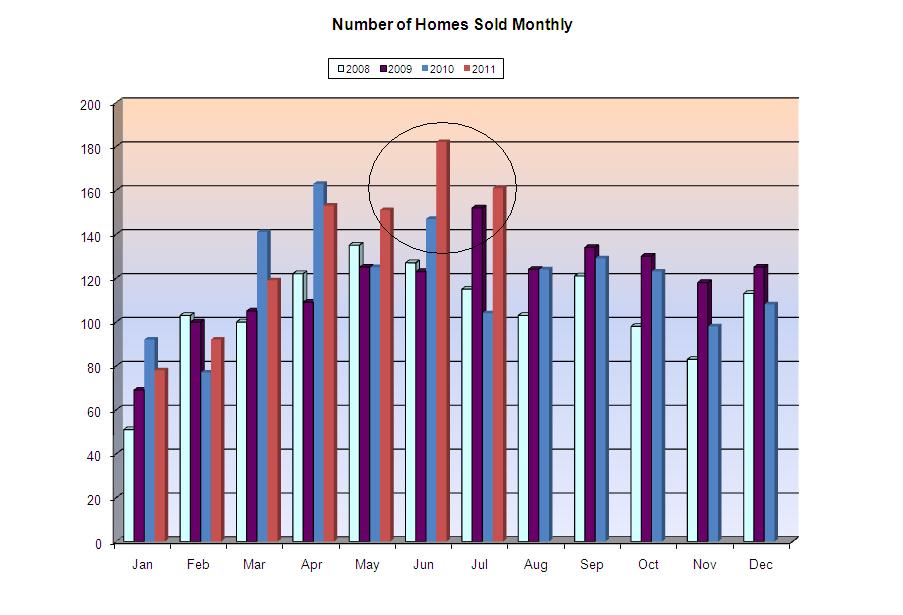

Palm Coast, FL – August 10, 2011 – Under the cloud of a world financial crisis and a disfunctional federal government in Washington DC, Palm Coast and Flagler County home sales show consistent improvement. There were 161 single-family homes reported sold through MLS during July; up 54.8% over the 104 homes sold in July 2010. The median selling price was $124,500, down slightly from July 2010’s $133,500. But the total value of all July 2011 home sales transactions still exceeded July 2010’s total by 50%.

July completes a three-month run of impressive year-over-year gains. For the three month period (May – July), the number of homes sold increased 31.4% while the total value of sales increased 23.4%. The market continues to be dominated by distressed properties and driven by cash sales. Intrestingly, cash sales were evenly distributed between distressed and non-distressed homes.

|

# Homes |

Median Price |

Days on Market |

|

| Lender-Owned |

37 |

$106,000 |

86 |

| Short Sales |

42 |

$100,000 |

192 |

| Non-distressed |

82 |

$141,250 |

115.5 |

| Cash Purchase |

85 |

$120,000 |

114 |

Inventory

The inventory of homes available for sale continued its downward trend. Inventory is bouncing around in the 1,065 to 1,075 range. There were 1,166 homes listed at the beginning of June and over 1,200 at the beginning of May. That’s about 7 months worth of inventory at current prices; still slightly into the "Buyer’s Market" level.

Pending Sales

Condominiums

GoToby.com recorded thirty condo sales during July, about the same as last year. The median price was $228,000, well above median home prices. Palm Coast’s condominium sales are predominately from the upscale second home/investor market. Several sales were recorded in Hammock Beach, Cinnamon Beach, Yacht Harbor Village, Canopy Walk, and Tidelands. After a few Hammock Beach Club one-bedroom units sold in May for under $100,000, investors took notice. Several have since been sold for over $100K. The condo market has taken a greater hit, with current selling prices ranging from 50% to 80% off peak values. But the short sale foreclosure process and cash buyers have combined to deal effectively. The necessary step of flushing out distressed inventory is well underway.

Toby’s Forecast

I stand with my forecast over the past few months. The reduced inventory of properties available for sale will ultimately cause prices to rise. The number of units sold does not directly influence the buyer’s psychology so long as they continue to perceive that the property they don’t buy today will still be available later. But eventually, buyers will return to an earlier opportunity only to find that it has evaporated. Somebody else bought it. That lost opportunity will change their mindset, making them more likely to act more promptly. The sense of scarcity will start competitive juices flowing. Prices will begin to rise.The Palm Coast market shows more strength than the market as a whole. Distressed properties continue to make up about half the local housing market. But buyers flush with cash are readily available to snap up attractively priced properties. I spoke with two investors at a recent foreclosure auction. They told me that they have been successful remodeling selected distressed properties (installing upgraded countertops, cabinets, flooring and appliances) then reselling them. They commented that real bargains were getting harder to find.

There were 457 pending and contingent sales as of the end of July. Pending sales have dropped from a high of 545 in mid-June. The drop signals the arrival of the seasonal downturn in real estate transaction volume.

Newswatch

Of course, the current mess in Washington continues to cast a shadow over the housing recovery. Here’s a list of things to watch:

- Mortgage Interest Deduction – Some lawmakers still feel that eliminating the mortgage interest deduction will help balance the federal budget. The loss of the deduction would negatively affect the housing recovery.

- Credit Availability – Overly strict mortgage loan underwriting practices and appraisal guidelines are making it very difficult to obtain mortgages, even by credit-worthy buyers. Hence the reliance on cash driven sales. Imagine our local market with normal credit availability.

- National Flood Insurance Program – The National Flood Insurance Program is set to expire AGAIN at the end of September. Congress seems unable to grasp the key role this program plays in housing markets accross the country and especially in Florida. More than 5.6 million American home and business owners rely on flood coverage. They recently failed to grant an extension to December 31, 2011. A short-term extension is likely, but it will mark the ninth such extension since the original expiration date in 2008. A long-term solution is critically necessary.

Sales Forecasts

How will the bancrupcy of PMI, the isurance company for buyers effect the market. Buyer with less than 20% down will have a harder time getting mortage insurance. That inturn will impact sellers availability of buyers. And what will banks do about current customers who have PMI insurance if they go under. The stock exchange is also going to delist PMI as it stock price has fallen from $54.00 per sahre to $.41 per share last week.