First-time Homebuyers Absent from Housing Market

Millennials stay in school longer, get married later and start families later or stay single. With crushing college loans, a weak job market and tight credit standards, they rent rather than buy.

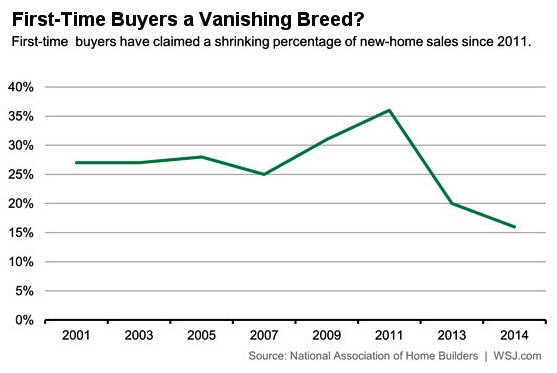

Palm Coast, FL – June 30, 2014 – First-time homebuyers have played an important role in past housing recoveries. Not so this time around. According to the National Association of Home Builders, first-timers have accounted for only 16% of new-home sales so far this year, as opposed to 25% to 28% from 2001 to 2007. To understand why, look to the Millennials.

Palm Coast, FL – June 30, 2014 – First-time homebuyers have played an important role in past housing recoveries. Not so this time around. According to the National Association of Home Builders, first-timers have accounted for only 16% of new-home sales so far this year, as opposed to 25% to 28% from 2001 to 2007. To understand why, look to the Millennials.

Millennials, those born between the early 1980s and the early 2000s, are not much like their parent or grandparent Baby Boomers who were born in 1946 through 1964. The behavior shift over one or two generations is stark, according to a recent CoreLogic report.

Millennials have achieved a higher level of education, staying in school longer than preceding generations. In 2013, 34% of Millennials had bachelor’s degrees vs. 24% of Baby Boomers when they were the same age. But many Millennials left school with unprecedented levels of debt, facing a weak job market and strict home lending criteria.

Many have chosen to rent rather than buy a home. In 1980, the homeownership rate for Baby Boomers aged 25-34 was 51.6%. The rate for that same age group in 2012 was only 37.9%.

“The rise of educational achievement has been occurring steadily and started well before the Great Recession began in 2007. Educational attainment is theoretically an investment in future income earning capability, so the fact that Millennials are more educated than prior generations should prove beneficial for their ability to become homeowners in the long term,” the report said.

Marriage has traditionally been a factor driving first-time homebuyers. The share of Millennials who are married was 26% in 2013. At the same age, 36% from Generation X and 48% of Baby Boomers were married. In 2012, 36% of Millennials were living with their parents.

The economic whammy facing Millennials is summarized in CoreLogic’s report saying, “Since Millennials are becoming more educated and delaying household formation, their labor and balance sheet profiles are on lower trajectories relative to previous generations. According to new Federal Reserve research, Millennials are less likely to be in the labor force and have half the net worth of Generation X and Baby Boomers at the same age, a massive difference.”

Meanwhile, the number of Baby Boomers reaching retirement is exploding. Those who weathered the Great Recession are paying off their mortgages or selling their homes to pay cash for down-sized housing. This trend will drive the market for the next two decades.

More economic problems than getting a mortgage.

At the height of the last housing boom, people seeking mortgages did not have to prove their income. A decent Fico score landed you a mortgage. The acceptable Fico score went as low as 500. Also, people were buying homes with no money down.

All forms of regulation ceased to exist, starting with Reagan, when builders could get loans with no money down. Recession in 1981, they all went bust, the government bailed out the S&L’s, The Resolution Trust Corp. was formed. Clinton was the master deregulator, and the few left, were deregulated under Bush. Easy credit, a housing boom, no regulation, this catapulted America into the Great Depression of the 1930’s. The idiots in Congress, let history repeat itself. Hoover was of the opinion that the markets would regulate themselves. When Greenspan gave his final report to Congress he openly admitted, that the markets would regulate themselves, and he had left interest rates too low for too long.

Since Greenspan we’ve had Bernanke, and now Yellin; the interest on the $17 plus trillion dollar debt has been at 0%. This is an experiment perpetuated upon the American people. The research I’ve done constantly comes to one conclusion. The Federal Government will eventually repudiate the debt, and the US will no longer be the world’s reserve currency. Already our US bonds have been downgraded.

Economically we are headed into real trouble, when the US Government goes belly up we will all be affected.