The Government’s Incredible Shrinking Mortgage Mod Program

In September, for example, banks modified almost 28,000 loans, but nearly 10,000 homeowners fell out of the program because they defaulted on their modified payments.

Palm Coast, FL – October 28, 2010 – The U.S. government’s effort to help struggling homeowners is approaching a standstill, and the number of homeowners in ongoing mortgage modifications could start shrinking in several months if current trends continue, according to a ProPublica analysis of Treasury Department data.

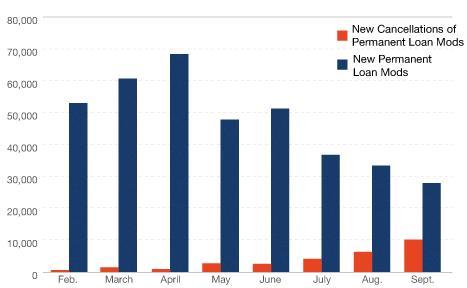

A year and a half into the program, the number of homeowners defaulting on their modified loans has been fast approaching the number of new modifications. In September, for example, banks modified almost 28,000 loans, but nearly 10,000 homeowners fell out of the program because they defaulted on their modified payments. Taken together, the programs’ growth has slowed by almost a quarter each month since May. The administration launched its foreclosure-relief effort last spring, looking to help 3 to 4 million homeowners by modifying their mortgages to have affordable monthly payments. Only 467,000 homeowners are in modifications that are still ongoing.

Alan White, a law professor at Valparaiso University, said the problem isn’t the rate at which homeowners are redefaulting, which is low compared to other modifications, but rather the shrinking number of new modifications given out by banks. "We need to be modifying 10 times as many a month," he told us.

Across the country, over 5 million mortgages are more than 60 days overdue or in foreclosure, according to Lender Processing Services.

Banks have had a poor record of modifying mortgages under the government program. (Check out our graphical breakdown of each bank’s performance.) Homeowners report Kafka-esque experiences of lost paperwork, miscommunication and dashed hopes in trying to get help preventing foreclosures. We’ve recently chronicled homeowner experiences in a series of profiles and a questionnaire. Investors who own mortgages are dismayed as well. The Treasury Department has yet to penalize a single mortgage servicer since the program launched last spring.

Source: Making Home Affordable monthly reports

Source: Making Home Affordable monthly reports"You start with a program that’s not well designed and a lack of will to enforce the program, and this is what you’re getting," says White.

The pipeline for permanent modifications also continues to dwindle. There are now fewer than 175,000 active trial modifications, down from almost 260,000 in July. Nearly half of the active trials are at least six months old.

We contacted Treasury to ask about the slowing of the program, and they haven’t responded yet. We’ll update this post when we hear back.

Two mortgage servicers, Bank of America and Aurora, have seen their numbers of active permanent modifications decrease in the past month. Bank of America’s dropped by about a thousand modifications, and Aurora’s fell by over 2,500 modifications.

In a press release, Bank of America said that the drop came from a combination of defaulted modifications, servicing transfers and repaid mortgages. Only 428 mortgages have been repaid to the more than 100 mortgage servicers participating in the federal program. Aurora did not respond to ProPublica’s request to comment.

Update: Treasury said it is working to reach as many eligible homeowners as it can and has expanded alternative options for borrowers that do not qualify for the modification program.

Source: ProPublica

Toby’s Commentary: I’ve heard from several individuals who feel trapped in the mortgage modification and foreclosure vortex. Lenders and loan servicers, swamped with problem loans, are utterly inept in handling individual borrower issues. I’ve heard from people who have spent hours on hold, only to be told that their paperwork cannot be found and to please resend it. Others have told how a modification commitment was expected soon only to find that their loan had been sold or foreclosed.

A new name in the business is IBM Lender Business Process Services or simply LBPS. Yes, it’s the same IBM. This business unit was formed in March 2007. Several of the larger banks have notifyed their borrower/clients that their mortgages have been sold to LBPS.

Google blogs. You will find that there is quite a bit of animosity developing towards this IBM unit and lenders in general. Lenders do not seem to realize they are sitting on a powder keg.

Leave a Reply

Want to join the discussion?Feel free to contribute!