Economic Indicators: Weekly Update – May 6

A weekly analysis of the economic data released during the past week, and how current economic conditions are affecting the real estate market.

Palm Coast, FL – May 6, 2011 – Every week the Research staff analyzes key data releases and explain what they mean for you and your business. In this update, we give the highlights of the most important data releases for the week of May 2-May 6, 2011, along with graphs that show the latest movement and overall trends.

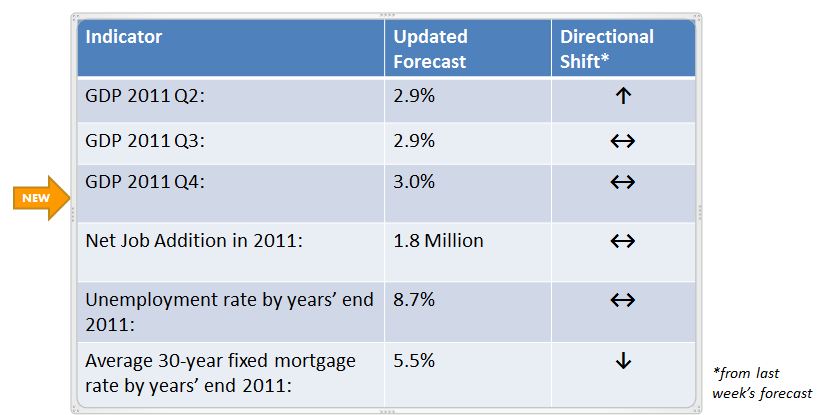

At a glance, this table shows the forecast for some of the most pertinent weekly data for REALTORS® to keep in mind. This changes from week to week as new data becomes available. The directional shift notes the trend from last week’s numbers. For the full forecast from the latest Pending Home Sales release, click here (PDF).

Highlights for Monday, May 2, 2011

-

The Nation’s manufacturing plants continue to show busy activity according to the latest industry survey of supply managers. The ISM index remained above the 60 for the fourth straight month, to April.

-

However, in looking at several components of the index, the industry expansion growth was the strongest in inventory accumulation and weaker in new orders. Meanwhile, inflation at factories is picking up as 72 percent of respondents indicated higher prices while only 1 percent said lower prices.

-

Construction spending, which measures completion of building projects, made its first gain in four months with a gain of 1.4 percent in March.

-

The latest manufacturing and construction activity points to a slight upgrade in GDP growth in the current quarter. First quarter GDP growth of 1.8 percent was weak, but the second quarter could be something closer to 3.0 percent.

Highlights for Tuesday, May 3, 2011:

-

The Census released new data on factory orders this morning which rose 3.0% in March, the 5thconsecutive increase. This increase was stronger than expected and reflected improved demand for both durable and non-durable goods.

-

March’s strong reading for factory orders indicates that despite rising fuel prices, supply-chain disruptions caused by the tsunami and nuclear crisis in Japan, and volatile consumer confidence, businesses expanded their pattern of investment in capital goods and consumer’s appetite for big-ticket items like automobiles remains strong. This trend is important as it suggests confidence on the part of business that will drive the expansion of the economy and hiring.

Highlights for Wednesday, May 4, 2011:

-

Mortgage applications rose 4.0 percent for the week ending April 29.

-

The Purchase index gained 0.3 from the previous week, but was 36.9 percent lower compared with a year ago. Refinancing activity accounted for most of the increase.

-

Based on the April ADP National Employment report, nonfarm private business employment increased by 179,000 jobs between March and April.

-

The Institute for Supply Management Non-Manufacturing Index reached 52.8 in April, a 4.5 point decline from March’s 57.3 percent. A level of 50 or higher indicates expansion in the services sector.

Highlights for Thursday, May 5, 2011:

-

New jobless claims surged again last week by 43,000 to end at 474,000. The four-week average was consequently up by 22,250 to 431,250 which is an almost 40,000 increase compared to a month ago.

-

The auto sector also suffered significant losses due to shutdowns and possible supply disruptions from Japan. Given the volatile month of April for jobless claims, tomorrow’s employment report will provide a clearer picture of the job market situation.

-

There were 1.3 million net new job additions in the past 12 months to March. If jobless claims stay up like they have in the past week and do not trend down, NAR expects less than 1.5 million net new jobs in the next 12 months, which would barely lower the unemployment rate.

Friday, May 6, 2011:

- Today’s payroll employment release showed growth of 268,000 private jobs in April which combined with a small loss of government jobs at the state and local level for net growth of 244,000 nonfarm jobs. This is the third consecutive month of private payroll employment growth well over 200,000 jobs and data from the previous two months were revised to show more employment growth. Job growth was wide-spread among industries.

- At the same time, the unemployment rate increased from 8.8 to 9.0 percent. An increase was expected at some point in the recovery as many who were discouraged and therefore not counted in the labor force reenter as they begin to search for work. Both median and average duration in unemployment declined.

- The economy has now recovered 1.8 million of the 8.75 million jobs lost during the recession. If this rate of job growth continues, the economy will recover the jobs lost in about 3 years. It will take longer at this rate, however, to create enough jobs to lower the unemployment rate because of the population growth that has occurred during and since the recession.

- Recent weekly unemployment claims were rising indicating that there could be a slower rate of job gains in May and/or June.

Source: National Association of Realtors® – Reprinted w/permission

Leave a Reply

Want to join the discussion?Feel free to contribute!