Best March Home Sales in Six Years – Absorption Rate Improves

A feeding frenzy has begun in the ”below $125K” price category.

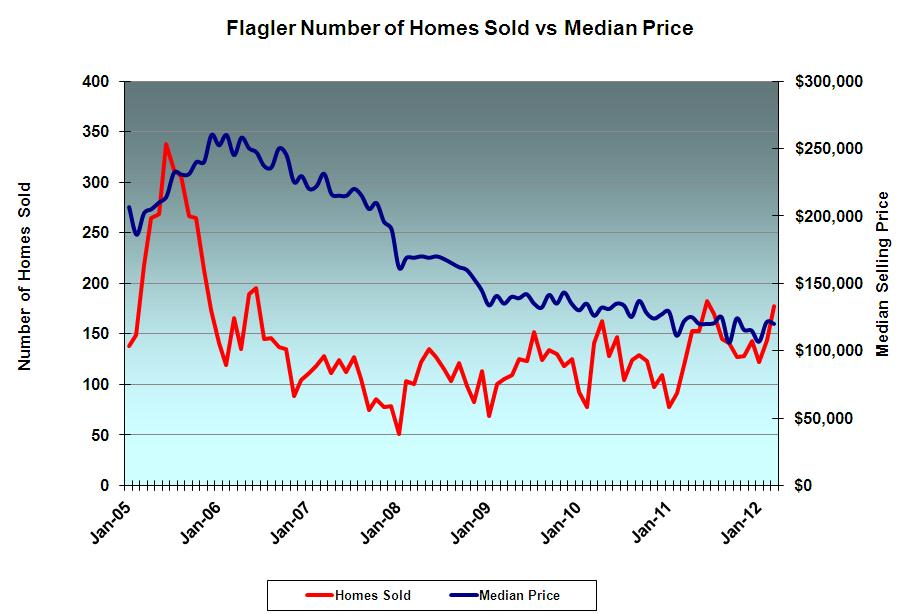

Palm Coast, FL – April 9, 2012 – Palm Coast/Flagler’s real estate market has definitely turned a corner. There were 178 single family homes reported sold (closed) via MLS in the county during March. That’s the most homes sold in March since 2005. It represents a 23.6% increase from February and a 49.6% increase from March one year ago.

There are only 866 MLS single-family home listings in Flagler County. At March prices and selling rate, that represents only 4.9 months inventory, well within the range industry analysts consider a "normal" market. The low end of the market is dominating. Only 195 of the listed homes are priced under $125,000 yet 102 homes in that market segment were sold during March; producing an absorption rate of 1.9, meaning that the inventory within that price range represents only two months of sales at current prices and sales volume.

Absorption Rates

Lower absorptioin rates indicate more brisk sales levels. Absorptions rates offer a good view of how different segments of the market are behaving.

|

Category |

Absorption Rate |

| Homes | |

| Belle Terre |

8.0 |

| Cypress Knoll |

6.0 |

| Indian Trails |

4.6 |

| Lehigh Woods |

3.6 |

| Matanzas Woods |

6.7 |

| Palm Harbor |

7.6 |

| Pine Grove |

2.1 |

| Pine Lakes |

3.2 |

| Quail Hollow |

1.8 |

| Seminole Woods |

3.6 |

| Grand Haven |

10.9 |

| All Flagler Homes |

5.4 |

| Condominiums |

|

| Canopy Walk | |

| Cinnamon Beach |

38.0 |

| European Village |

7.3 |

| Hammock Beach |

12.5 |

| Hammock Dunes |

36.0 |

| Palm Pointe |

0.6 |

| Surf Club |

4.4 |

| Tidelands |

1.6 |

| All Condominiums |

8.5 |

Distressed and cash sales continue to comprise roughly half of all home transactions. Eighty-six were distressed sales; either lender-owned via foreclosure or deed in lieu or short sales. That and unavailability of credit are holding prices down. Fully 50.8% of the sales were reported as cash transactions.

This is an unprecedented market. Traditional analytical tools are less useful. They were meant to measure market behaviors that no longer exist. So we resort to reading tea leaves; looking for nuggets among the data.

Median prices have stabilized, but have yet to begin to rise. But there are pockets within the market showing strong signs. Lender-owned properties are now typically receiving multiple offers with winning offers above listing price. Only 56 lender-owned single-family homes are listed for sale on MLS, representing barely one month’s sales in that category.

Agents and brokers tell me they are unusually busy with active clients, but fret that they are working twice as hard for half the reward. Commissions are halved by lower transaction values. Distressed properties require more intensive documentation and nurturing. Still many of them fail to close. Brokers are only compensated at closing.

Investors have definitely entered the market. Not too many months ago, my weekly transaction column documented sales at prices less than half the most recent sale which typically occurred in the 2004 to 2007 time frame. Recently, I’ve noticed an increase in the number of flipped transactions. Investors are selectively acquiring distressed properties that need a little tender care, making a small additional investment, and then reselling the homes.

Investors are also buying single-family homes and condos, then renting them. It makes sense that rentals are in demand. Those who recently went through a foreclosure or short sales will be unable to buy for some time, swelling demand for quality rentals.

Condominium sales are even more affected by the lack of credit. All but two of the 31 MLS condominium sales were reported as cash sales.

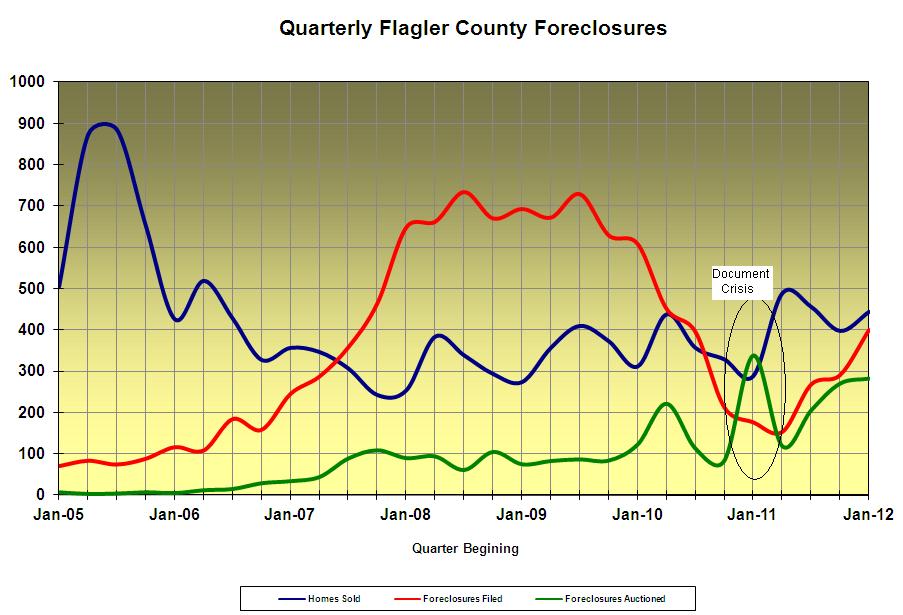

Banks are definitely more aggressively disposing of distresses properties, both by more quickly approving short sales and by aggressively pricing REOs. The number of foreclosure filings is on the rise, leading some pundits to proclaim a new wave of defaults. In fact, about 80% of recent filings appear to be re-filings of earlier defaults. When the robo-signing documentation crisis hit, many lenders were forced to withdraw foreclosures until they could create more believable documents. Having done that, they are now re-filing the same old cases.

Foreclosures peaked between mid-2008 and mid-2010. Many have reaching the final step in the process, the foreclosure sale. A record 282 properties suffered that fate in the first quarter of 2012.

Flagler and Volusia home builders recently completed their respective 2012 Parade of Homes. Both groups report more sales and potential buyers than in recent years. The mood is shifting. There is more optimism in the air; the kind of optimism that is necessary for a healthy housing market. Let’s hope that national and international economic woes don’t worsten.

Note: Statistics quoted in this newsletter differ slightly from those in my April 7th Palm Coast Observer article. My Observer deadline is 9:00 A.M. Thursdays for the Saturday edition. Meanwhile, March sales continue to be posted to MLS.

I think it is way too early…

The economy is going to slide again. This time more homes will hit foreclosure. The time will be right for buying when not only are lower value homes are selling but all categories are moving in that direction.

I tend to see what the rich are doing and many are selling their homes as quickly as possible. We as a nation have not seen the end of this downturn.

Snow Birds?

I have to wonder if this sharp rise in sales is not related to the greatly increased pool of snowbirds in Jan. Feb. and March?? We will see in the next couple months.

Reply to Craig

You are correct in that local sales are seasonal. That’s why I always compare results to the same month in previous years. There were more homes sold in March this year than in any March since 2005, when the bubble was fully inflated.