Why the Massachusetts Supreme Court Voided Two Foreclosures and What It Could Mean for Banks

While the decision’s impact isn’t entirely clear, even Wall Street analysts who downplayed its applicability, acknowledged its troubling implications for banks.

Palm Coast, FL – January 21, 2011 – When Massachusetts’ highest court ruled against U.S. Bank and Wells Fargo earlier this month and invalidated two foreclosures, the decision was hailed by some as an important precedent for courts seeking to resolve foreclosure disputes.

While the decision’s impact isn’t entirely clear, even Wall Street analysts who downplayed its applicability acknowledged its troubling implications for banks trying to foreclose with missing or insufficient documentation for the mortgage loans securitized and sold to investors.

The Massachusetts court, in its decision against the banks [PDF], ruled that in two very similar foreclosure cases, neither bank had been able to prove that it had the right to foreclose on the homeowner due to an incomplete chain of title. In other words, the banks couldn’t prove they had legal standing to foreclose because the transfers of ownership weren’t properly documented each time the mortgage changed hands—or was assigned to a new party—during the securitization process.

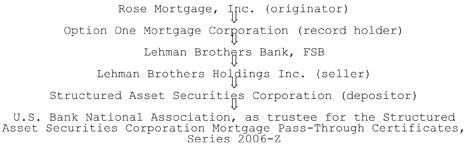

Here’s a handy chart from the ruling, showing how the chain of title should have been documented with the Ibanez mortgage:

U.S. Bank, as the chart shows, wasn’t the mortgage originator or the servicer in this case—it was the trustee of the mortgage-backed security (responsible for distributing funds to investors in the security). The Financial Times’ Alphaville blog explains how U.S.Bank’s documentation fell short:

One of the issues is the so-called "mortgage in blank" procedure. In the Ibanez case, for instance, the last mortgage assignment with a full set of names on it is from Rose Mortgage to Option One. After that, the mortgage is assigned in blank throughout the securitization. There’s no assignment with "US Bank" on it anywhere, though the bank did try to go back and finish off the assignment after it moved to foreclose.

Banks, in order to smooth over the problem of missing assignments, will often do “confirmatory assignments” after a foreclosure has been initiated. It’s standard practice in Massachusetts, FT Alphaville reported.

But these “confirmatory assignments” only work when “there is a prior valid assignment to confirm,” bankruptcy lawyer and foreclosure expert Max Gardner explained to me. Even though the lower court gave both banks time to produce evidence of earlier assignments, the banks weren’t able to cough up the proof.

They did, however, produce some securitization documents that the court said did not suffice as proof of legal standing in this case. U.S. Bank submitted the offering documents for the mortgage-backed security, which the court said showed an “intent to assign mortgages to U.S. Bank, not proof of their actual assignment.”

The court went on to say that even if the banks had produced a trust agreement or pooling and servicing agreement—proof that a mortgage pool was sold and assigned to the trust—they would still have to provide records detailed enough to show that the actual mortgage in question is contained in that mortgage pool.

The American Securitization Forum chose to take a glass-half-full approach to interpreting the ruling. It issued a statement saying it was “pleased that the Court validated the use of the conveyance language in securitization documents as being sufficient to prove transfers of mortgages” under Massachusetts law.

(Georgetown University associate law professor Adam Levitin, meanwhile, looked at securitization documents for other mortgage securities and concluded that many would probably fall similarly short.)

Wall Street has nonetheless argued that the Massachusetts ruling was limited in scope. Paul Jablansky, an asset-backed securities strategist at the Royal Bank of Scotland, issued a report stating that “we do not believe that this case will be a broadly applicable landmark.”

That could be true. The ruling only has direct implications for foreclosures in Massachusetts, and state courts elsewhere could rule differently on a similar set of facts. That’s up to the courts to decide.

CNBC points out that the problems may be close to impossible for the banks to fix. Take the Ibanez mortgage as an example—the chain of title was supposed to include assignments to and from Lehman Brothers, which collapsed in 2008:

Getting someone at Lehman to go through the process of executing the assignment is going to be very difficult. It’s not even clear if anyone at Lehman Brothers has the legal authority to execute an assignment now, while Lehman is bankrupt.In any case, getting the assignment from Lehman wouldn’t really help you. You’d still have a gap in the chain from Option One to Lehman. It’s probably best to skip over Lehman all together and go directly to Option One to ask for the assignment.But you have a bit of a problem. You didn’t buy the mortgage from Option One. They aren’t under any contractual obligation to you to execute any documents.

On top of that, the basic rules of securitization could be another obstacle for banks hoping to fix their mistakes by simply assigning mortgages years after the fact. The trusts were formed under tax rules passed in 1986 that gave them tax-exempt status so long as they “do not acquire any new assets after the trust closes,” according to FT Alphaville.

If the trusts violate these rules, they could potentially be required to pay penalties, taxes and interest, Gardner told me—ultimately wiping out investors.

No one’s sure what the Ibanez ruling will mean just yet, but one thing is clear: Foreclosing on mortgages that were securitized with insufficient documentation will continue to be tricky business for the banks.

Source: ProPublica [1-20-11]

How can I tell?????

If I am planning to purchase a house with previous mortgage on the property, how can I determine if that mortgage was securitized and the seller has legal rights to sell the house?

Yes, I am aware of the title insurance protection, I choose not to depend on that single insurance company’s financial health.